Pros & Cons of Stocks

Pros

- Most are easy to buy and easy to sell

just make sure you check the trade volumes & bid/ask spreads before you invest as this will give you a gauge of liquidity.

Large daily volumes and narrow bid/ask spreads are desirable.

- Some provide a Cash flow

Many pay dividends which helps increase the probability of a profitable investment. It puts a kind of floor under your returns

- Tax advantages.

Holding an investment for longer than a year qualifies you for long-term capital gains (rather than short term capital gains) and a lower tax rate on your profits.²

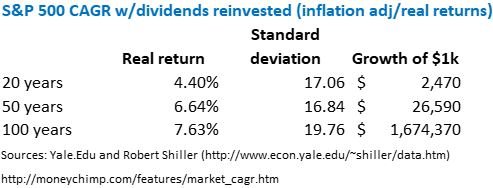

- Good historical returns that beat inflation

If you invest in stocks over long periods of time, it is quite likely that your purchasing power will increase at a pretty good rate (4-8%).

- Many low-cost options available

You can get decent returns through low cost ETF’s and mutual funds. Commission free trades are standard for most stock trades these days.

- Diversification as a part of a portfolio of many assets

Stock returns are uncorrelated or lowly correlated with many different assets. Investing in stocks as part of a multi asset portfolio is nearly certain to increase your risk adjusted returns versus a portfolio without stocks.

Cons

- See list of risks

There are ways to reduce or even eliminate some of these risks. You can never eliminate all risks.

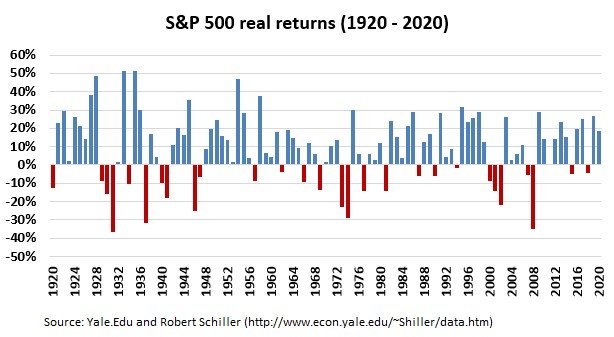

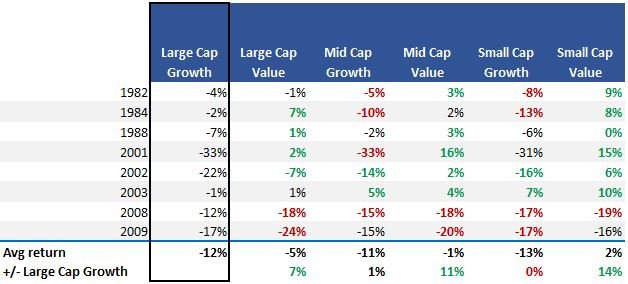

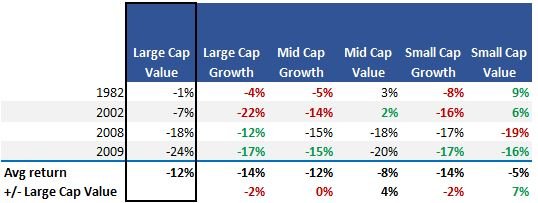

- Quite volatile

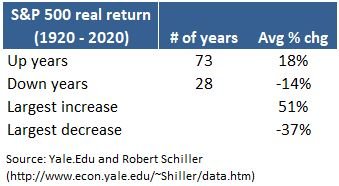

As you can see in the chart above, the variability (as measured by standard deviation) has been 3-4 times more than the return received.

In investment lingo, your risk/return ratio is less than one.

- You can lose money, including your entire investment.

As a matter of fact, it’s likely that you’ll lose money on several of your investments the longer you invest.

- It takes time. In more than one way

First, It takes time to research an investment. Because of the thousands of options, it’s easy to get overwhelmed and spend a ton of time trying to find the “perfect” investment.

Second, you gotta be patient. In any given year you can receive returns that are either low or downright negative. Hell, in any given 2-10 year period you can receive low or negative returns. It’s unlikely but is possible.

The best approach for most people is to invest over the long term which, by definition, takes time.

- You’re competing with bots/algorithms

Because there is so much money to be made, large investors such as hedge funds, banks, institutional investors etc., have written computer programs to take advantage of what seems like every possible opportunity in the market.

This can negatively affect you by reducing your returns.

A metric you have no idea about hits a certain threshold and triggers their bots to sell.

- Stockholders are paid last when company goes bust¹

Out of the last 100 years, the S&P500 has generated positive real returns in 73 of those years. The average real return was +18%/yr. Because of this long track record of consistently positive real returns, anyone with money invested should have a portion of their portfolio invested in stocks.

The appropriate percentage for your portfolio depends primarily on 3 areas:

- Returns you need to meet your goals

- Risks and chances of loss you are willing to accept in order to obtain that level of returns.

- The diversification benefit you can realize by adding stocks to your portfolio.

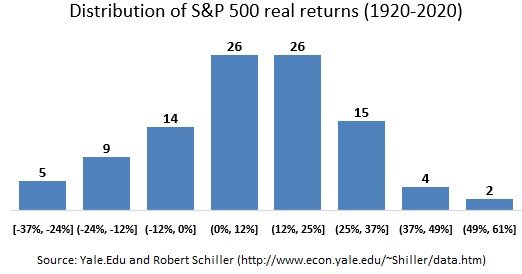

As I mentioned earlier, it is overwhelmingly likely that you’ll receive positive real returns in any given year. But you better be willing and able to accept losses when investing in stocks.

Here are a few charts to help you get an idea of the returns you are likely to receive if investing over the long-term.

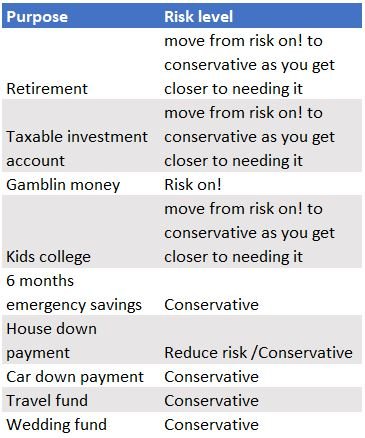

What is the $ for?

Money that is needed in the next 2-3 years should probably be held in more conservative investments such as high yield savings accounts or money market mutual funds/ETF’s.

Down payments on a car or house, savings for children’s college that will be used in the next year or two, savings for your upcoming wedding, a travel fund etc., are all instances where you’d want to be more conservative with that money.

Your ability to be conservative with the money is highly dependent on the inflation rate.

If inflation is not a problem and you can maintain your purchasing power by keeping the money in ultra-safe investments, then it’s usually the best to do so.

On the other hand, if the prices of the items that you intend to spend the money on are increasing faster than the interest rate you’re receiving in conservative investments, then you almost have to consider keeping at least a portion invested to try to maintain your purchasing power.

The percentage is up to you but in most circumstances it’s probably smartest to keep at least 40-50% in safe investments unless inflation is super high, like 10% or more.

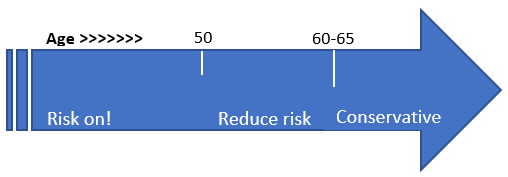

How long until you need the money?

If you are young and don’t need the money for a long time (retirement money), then mathematically speaking, you can afford to have a fairly large portion of your portfolio allocated to riskier investments offering higher returns.

If you receive poor returns for a few years (even 5 years), you’ll have plenty of time to recover.

The older you are, or the closer you get to needing the money, the generally accepted wisdom is to reduce risk. It’s wise to allocate a smaller portion to riskier assets and to increase your allocation to safer assets like cash, money market funds and/or bonds.

Can you stomach the risk?

Are you a person who can ignore market fluctuations and hold on for the long term?

If so, there is nothing wrong with taking on risk in pursuit of higher returns. As always, make sure you understand the risks and have a backup plan incase it backfires and ends up costing you money that you should have been protecting.

A useful exercise is to ask yourself, If I lost 40% of this money:

- Would it severely affect my daily financial situation?

- Would it cause undue stress and negatively affect my health or happiness?

- Would it jeopardize the goal for which I’m investing?

If you answer yes, to any of these questions it’s probably too much risk for you.

Ask yourself the same questions if you lost 25% of the money, and again if you lost 15% of the money and so on.

Generally, you have to be willing to take a 30% loss to invest in the stock market. Most of the time you will make money, especially over long periods of 10 years or more, but big losses do come around once every 10-15 years.

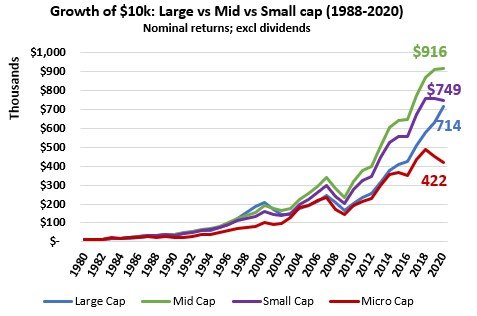

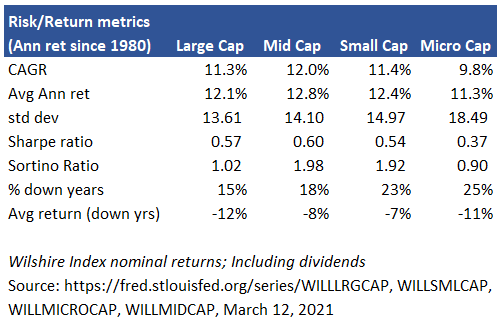

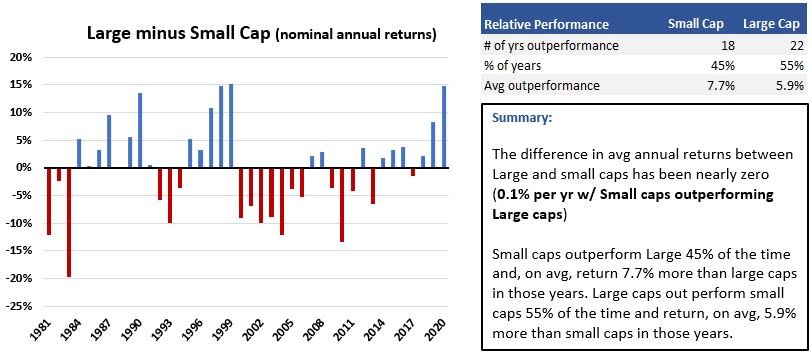

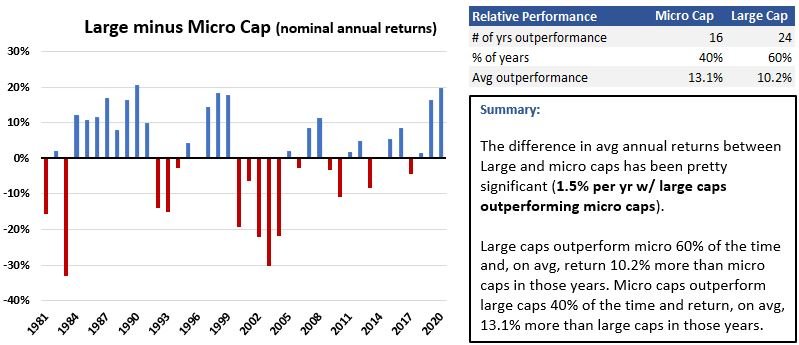

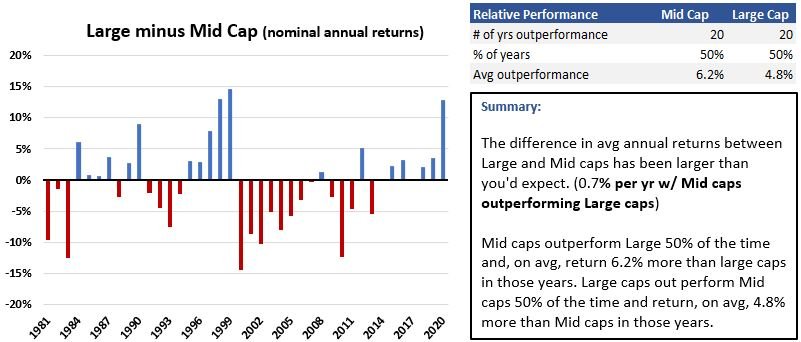

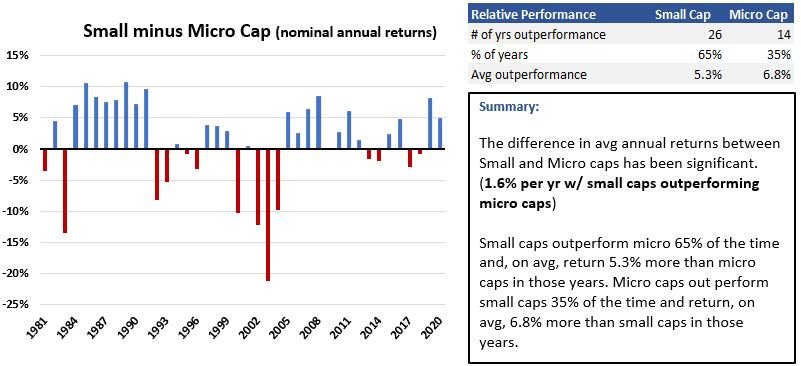

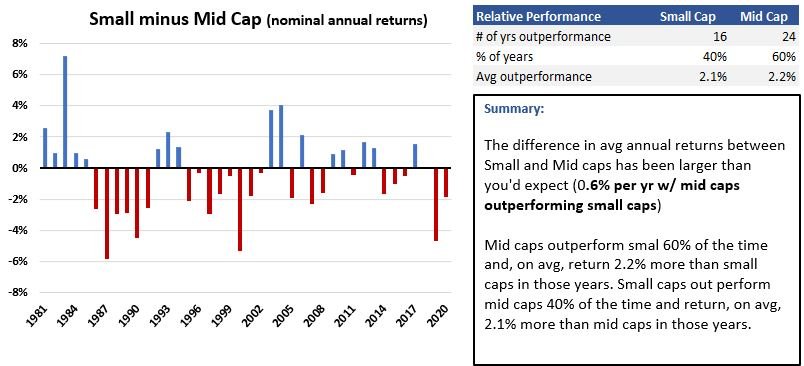

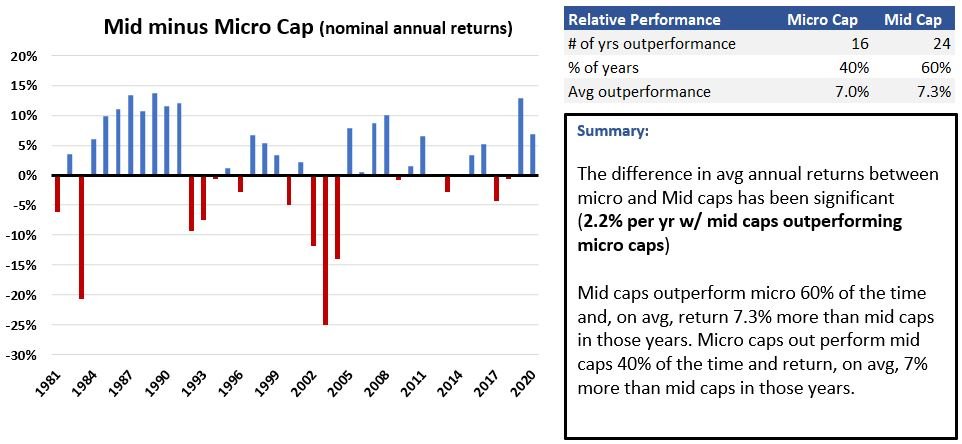

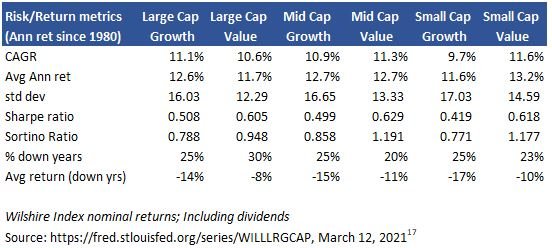

Size

You’ll usually hear people claim that the expected return increases as you go down the size spectrum. This has some truth but is not necessarily the case and is highly dependent on the time frame that you choose.

Since 1980, Mid caps have lead the pack on a total return and risk adjusted basis. And it’s not just the Compound Annual Growth Rate (CAGR) over this 40 year period. Mid cap beat all other sizes over 3, 5 & 10 year rolling periods.

There is one caveat. Large cap has mopped the floor with all of them the last 7 years by an average of 4.6%/yr over small, 6.7%/yr over micro and 3.4%/yr over Mid! (Primarily on the backs of the Facebook, Google, Amazon and Microsoft cartel + Netflix.)

As a matter of fact, the outperformance of Mid-caps over the 40-year period shown above is not statistically significant vs large or small caps. This is a reminder that past returns are not a guarantee of future returns and that any of the categories can outperform the others in any given day, week or year. So, do your own research before making any investment decisions.

However, such a large outperformance warrants the consideration of increasing your allocation to mid-caps, especially for longer term investors.

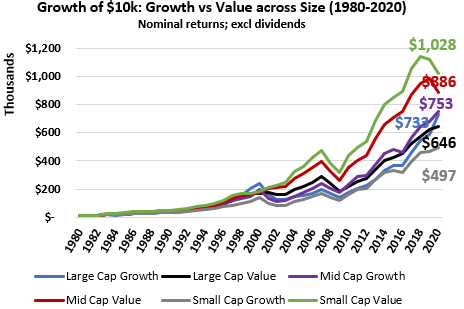

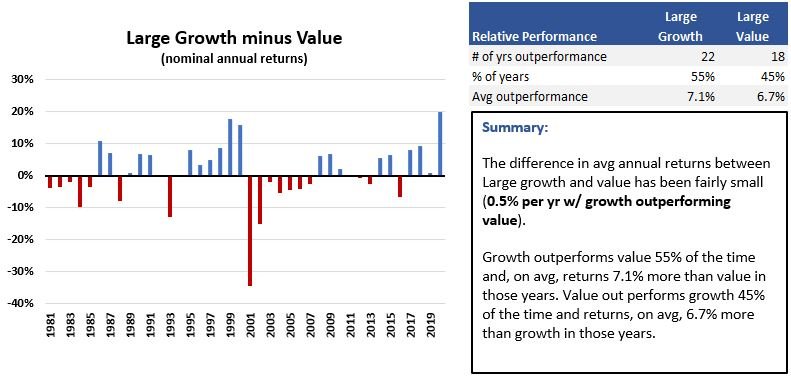

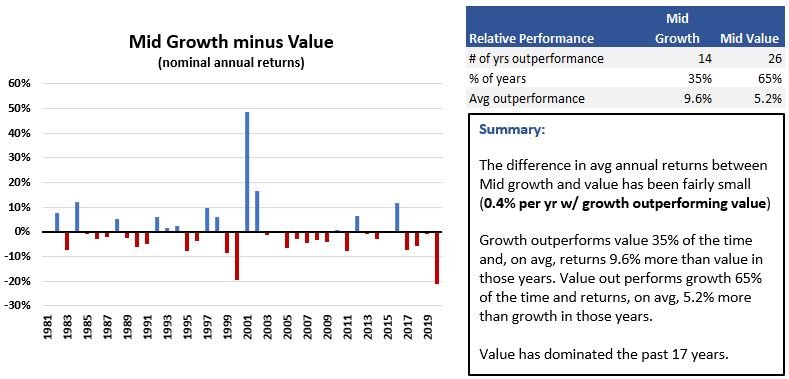

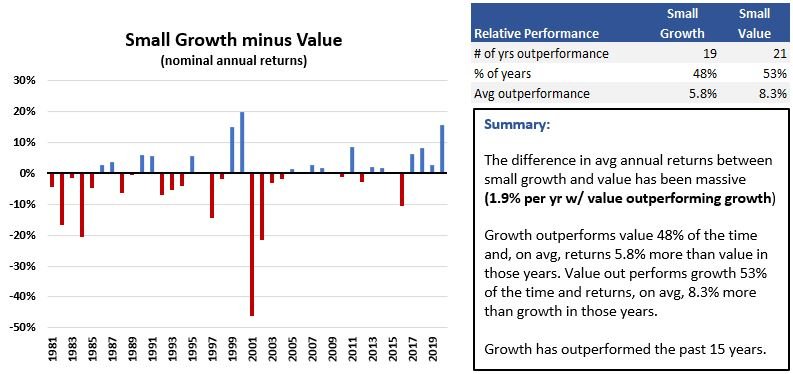

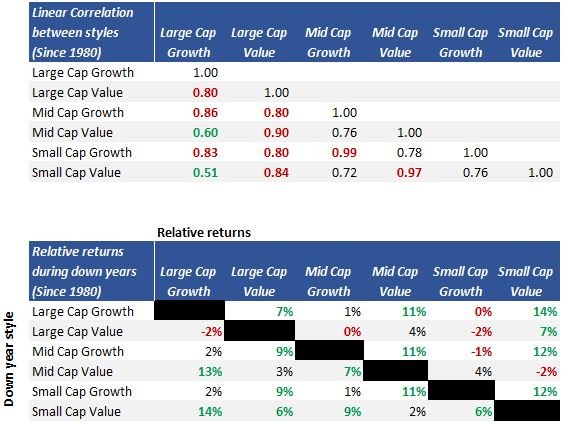

Style

As a reminder, when we refer to a stock’s “style”, we’re talking about whether it’s a growth stock or value stock. You’ll also hear about a blend of the two, usually when investing in mutual funds or ETF’s.

On a risk adjusted basis mid cap value nudges out small cap value due to lower price volatility. But on a CAGR basis, Small cap value has performed the best since 1980.

There is one caveat. Large cap growth outperformed all of them 6 of the last 7 years primarily on the backs of the Facebook, Google, Amazon and Microsoft cartel + Netflix.

Geography

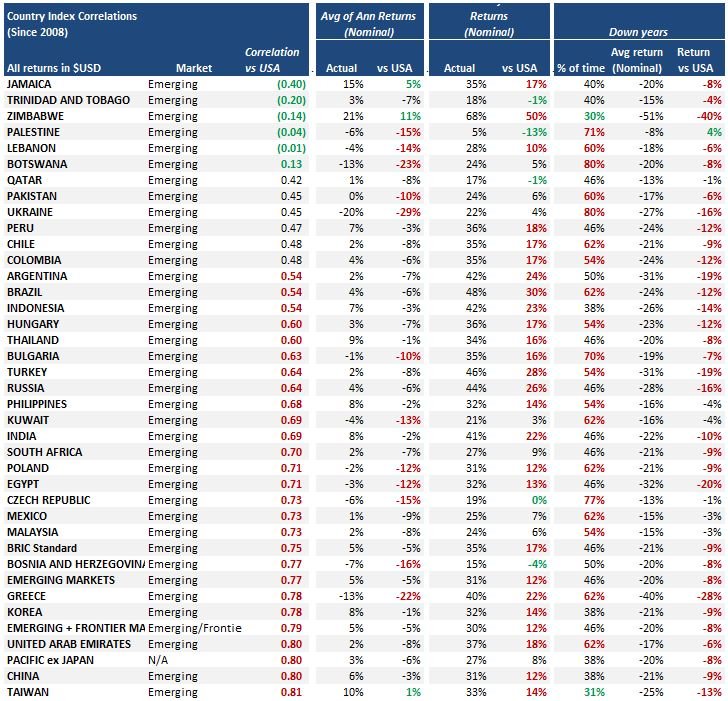

Based on the above data, it seems to me that there are only a few countries worth taking a look at. They’re the ones that have a low enough correlation to US stocks and a high enough return to be worth the additional risk.

Surprisingly, the two most obvious candidates are…GULP…..Jamaica and Zimbabwe!

I honestly didn’t think I’d find this.

- Jamaica – Get a 15%/yr return to potentially lose 20% of your money more than 1 out of every 3 years?

- Zimbabwe – Trade a 21%/yr return for the risk of losing 51% of your money (!!!) about 1 out of every 3 years?

- Taiwan – Accept a high correlation with US stocks in exchange for 10%/yr returns and a chance to lose 25% of your money about 1 out of every 3 years?

- Romania – 7%/yr returns with an even higher correlation to US stocks in exchange for a 7% loss every two years?

- Denmark – 12%/yr returns with a still higher correlation to US stocks in exchange for a 25% loss about 1 out of every 3 years?

The primary purpose of investing internationally is to not only goose your returns but to also hold an investment that is uncorrelated or lowly correlated to US stocks. If you can’t get an investment that is not correlated or at least very lowly correlated to US stocks, what is the point of taking the extra risk?

We will explore the diversification benefits in the next section, but you can clearly see from the data that there are only a couple options worth considering.

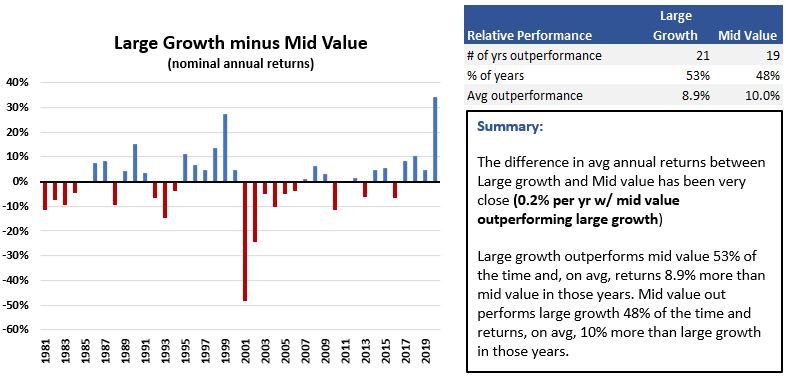

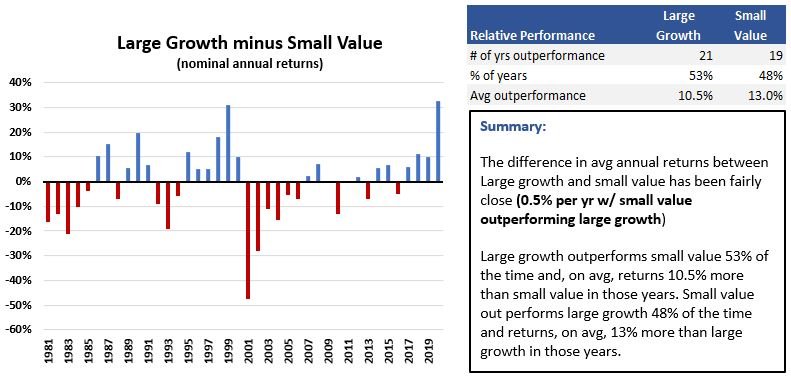

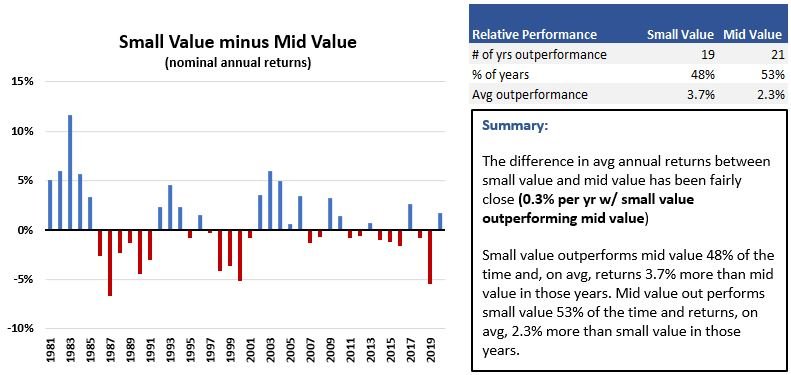

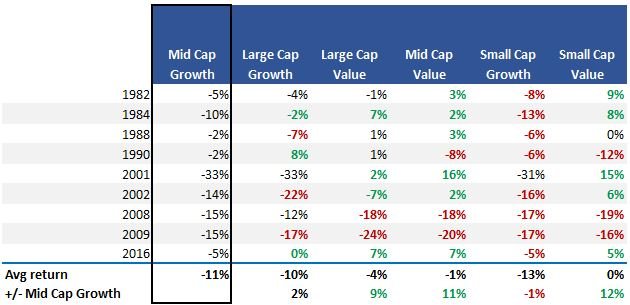

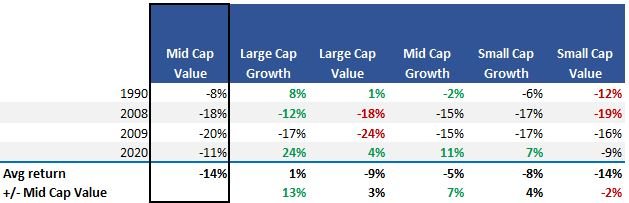

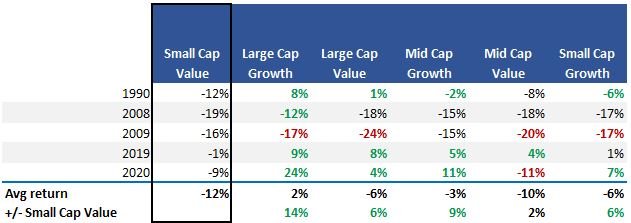

Style

The churn is real! The correlations between cap sizes within a given style (i.e. growth vs growth or value vs value) are very high and performance is fairly close during down years regardless of the cap size.

In other words, when growth is down, all sizes under growth are dragged down and vise versa.

Similar with the value side, but value appears to hold up a little better between the cap sizes than growth does.

Out of all the styles, the two that seem to provide the best diversification are Mid cap value and Small cap value.

Not only do they have very low correlations to the growth side, they kill it when growth is down, and they hold up when large cap value is down.

There is one large caveat here. When it comes to financial collapses like we had in the Great Financial Crisis, everything goes down with very few exceptions. From the data I’ve seen, only a couple of assets protected you from declines in 2008-09 and again in the Coronavirus flash crash of 2020…… Cash and US Government bonds.

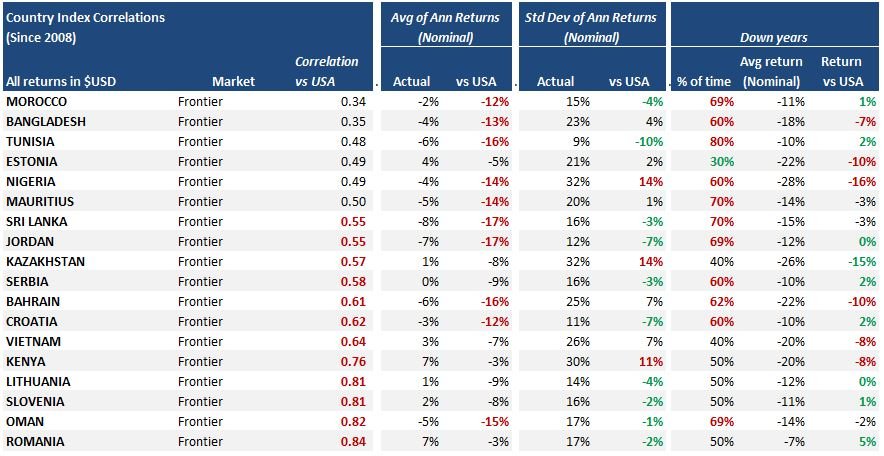

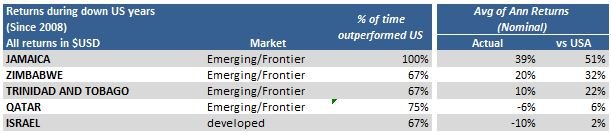

Geography

Based on the above data from MSCI, almost all negatively or lowly correlated countries are emerging or frontier markets.

That’s one of the things that bugs me about international mutual funds and ETF’s. They tout diversification as a benefit of their investments, but a large majority are stacked with companies from countries that have very high correlations to the US (United Kingdom, France, Italy, Germany etc).

You’re not getting the diversification you think you are by investing in international funds or ETF’s. It’s mainly a marketing scheme.

If you want true diversification through low or negative correlation, you gotta go with Emerging or Frontier markets.

How about performance during down times in US stocks?

For 89% of the country specific indexes, they performed the same or worse than that US did.

Yet another data point suggesting that geographical diversification does not appear to increase overall returns of a portfolio. At least not since 2008 and through the indexes I’m using.

There were a couple countries that did stand out and almost all of them were emerging and frontier markets:

- Jamaica – Once again Jamaica stands a top the list. And this wasn’t just one big year vs the US. Not only did it beat the US in all 3 of the last US down years, they outperformed by an average of 51%! And returns were heavily positive in all 3 years.

- Zimbabwe – Another notably uncorrelated country, but the average return is heavily influenced by a +96% year. Go ahead and take your chances but be prepared to get kicked in the teeth

- Trinidad & Tobago – The 2nd most uncorrelated country to the US has performed quite well the last 3 US down years. And the year that it didn’t outperform the US, they only lost 5% vs -1% for the US. Not like you lost 20% or something. The only caveat is that in all years, their return is nothing to write home about so take what you will from the fact that they have done well the past 3 US down years.

- Qatar – Similar to Trinidad & Tobago in that it is highly uncorrelated to the US and has outperformed the US in each of the last 4 down years, including the great recession. The avg annual return in all years since 2008 is a measly 1% and almost 50% of those years were down years. Put that mouth guard in if you decide to invest here.

- Israel – the only developed market to beat the US in more than 2 of the last 4 down years while also outperforming the US by an average of 2%/yr in those years. Don’t pass up the -31% return in a year that the US only lost 1% though. Another mouth guard country.

Investing in emerging and frontier markets is a call you have to make for yourself.

Of course, there are other factors you should investigate before investing in these types of countries (See the list of major risk factors above).

One caveat to this analysis is that I’m using MSCI indexes as proxy for the most probable returns you could expect because they are the primary benchmark used for many ETF’s and mutual funds. However, there are thousands of funds and ETF’s out there that won’t have an investment mix anything like these indexes.

Therefore, before adding any investments in the name of diversification, analyze the specific investment in terms of correlation to the other investments in your portfolio. See if it helps reduce expected variability while not compromising expected return too much.