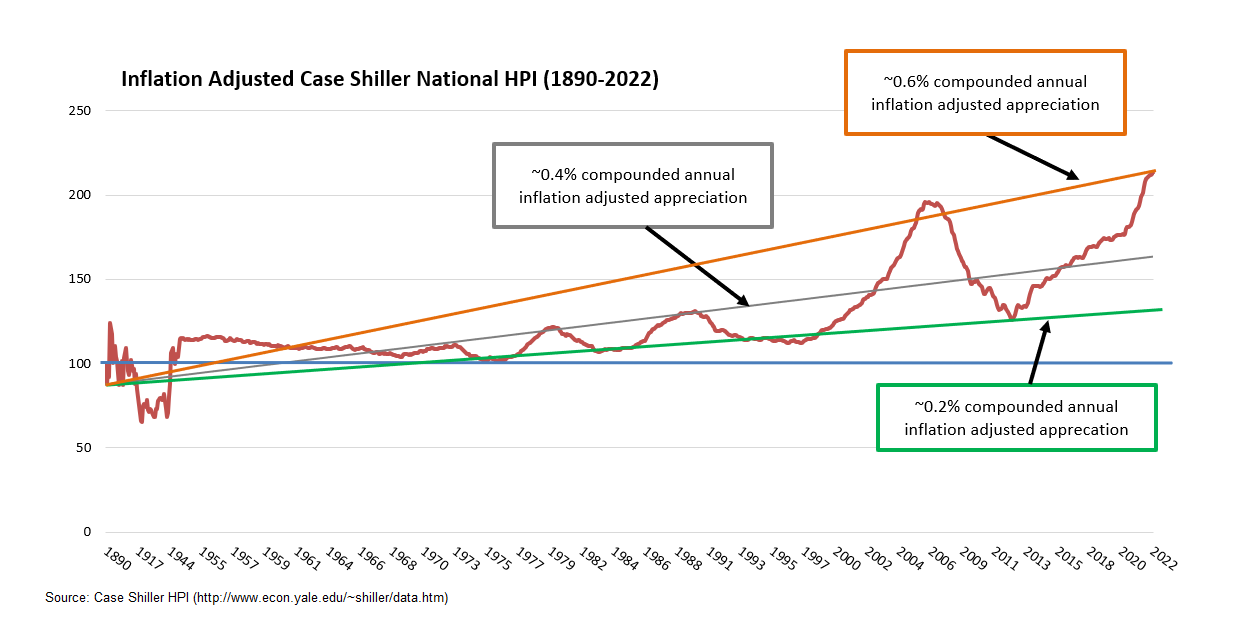

House Prices Adjusted for Inflation & Interest Rates

As we just discussed, the Case Shiller HPI is higher than it was just before the GFC. And it’s not just a few markets. It’s pretty much every single major metro area, even when you adjust for inflation & interest rates[2] – Two of the primary drivers of house prices.

Prices vs Incomes

There are 2 main measurements of house prices to income:

- Price to Income Ratio

At approximately 6, the median price to income ratio is higher than it has been going back to 1984.

2. Mortgage Payment as a % of Median Household Income

A mortgage payment on the median priced home as a % of median household income is the highest since 1990.

This shows the current payment on the median priced house consumes 36% of a median household’s income, higher than the peak of the GFC.[3]

The only other time in this data set that was higher was in 1984 when it was at 45%! This is possibly the highest reading ever, driven by sky high interest rates at that time.

If you think 36% is bad, it doesn’t account for Income taxes, property taxes, homeowners’ insurance, or mortgage insurance. If we add those in, we’d likely be looking at 50% or more of the median household income going towards housing costs.

Price to Rent Ratio

The Price to rent ratio is exactly what it says. You take the median price of a house & divide it by the median rent. This is important because it can give us a gauge of emotion in the housing market.

You generally have two choices when deciding where to live. You can either buy or rent.

When house prices diverge from rents, & people are making the decision to pay $500, $600, $700 more per month to own a home it can be a sign that people are basing their decisions on emotions rather than logic and financial planning.

This is a chart from the website Calculatedriskblog.com which is based on a 2004 study of the federal reserve.[4]

He uses the same approach that the Fed used to calculate the ratio through 2022. As you can see, we are back to the peak that we saw in 2006 right before the GFC.

Fear of Missing Out (FOMO)

Fear of missing out is the existence of unusually high demand due to the fear that they won’t be able to afford it if they don’t get in now.

In real estate, we look at 4 primary metrics to gauge buyer demand & sentiment:

- High Sales to List Ratio

As you can see, sellers have had to reduce their list price between 2-4% to sell their property since 2012. Starting in 2021, sellers have been able to sell their homes for more than their list price reaching a max of approx. 103%. An all-time high in this data set.

In addition to the high sales to list ratio, the % of homes that sold above asking is a whopping 60%. Over the 2012-2020 period, it sat at about 25%. That’s a doubling in the % of homes that sell for more than asking, signaling insane demand & FOMO.

2. % Price Drops

Over the 2015-2020 period, the avg % of homes with price reductions sat at ~12-13%. Since the start of 2021, that rate decreased to about 10% further supporting the notion that sellers had control of the market since 2021.

3. Days on Market

This trend of significantly lower days on market is obvious. Since 2012 it has dropped from 97 days to 16 ,an 84% decline! Of course, 97 days was recorded at a time when we were just coming out of the GFC, which is why it’s so high.

The normal days on market is somewhere between 45-60 days. The current rate of 16 days is a sure sign of excess demand.

4. % Pending within 2 Weeks

Couple the prior 3 metrics with an explosion in the % of homes entering pending sale status within 2 weeks of listing & it’s not hard to see the presence of FOMO in the housing market.

Unusually Low Supply

Low supply of anything, provided there is a demand for it, will push the price up. Furthermore, the price will explode if demand is high while supply is low.

We’ve already established the presence of excess demand for residential real estate. Couple that with extremely low inventory, & it’s no wonder why we only have 1-2 months’ supply of homes right now, which is a historically low rate.

In the years leading up to the GFC, which nobody will argue that we were not in a bubble at that time, we were running at about 4 months’ supply.

Now, I can hear some of you screaming at your monitor…..But Leif, the low supply will put a floor under real estate prices. This is true….for now.

You see, when the difference between the price a house can sell for & the cost of building that house increases, this gives a signal to builders to build more because the profit margins have increased. And build they have!

The chart below shows the total # of units under construction hit an all-time high going back to 1970.[5] This is inventory that will likely hit the market over the next 3-18 months & almost surely at lower prices. We are already seeing homebuilders discount their recently completed properties.[6]

This is the % of all home purchases by investors. According to RedFin, Investors bought a record 20% of all sales in Q1 2022.

The theory is that the proportion of investors is important because they’re more likely to be the first to unload their properties & stop buying more if the market starts to fall.

This is particularly true for flippers because they get clobbered if prices are falling. Rising or flat prices are required for their business model to work. Publicly traded companies like Blackrock & Blackstone must adjust the value of their assets to the current market value for their quarterly earnings reports. If prices start falling, this hurts their earnings numbers which has tons of downstream effects on their business.

However, the data doesn’t fully support this claim that investors flee at the first signs of trouble. It absolutely was the case at the beginning of the pandemic where you can see that investors fled like their hair was on fire. Historically Q2 is a time when investors are quite active. In 2020 that wasn’t the case. Their market share went from 17% in Q1 2020 down to 11% in Q2.

Investor market share did not fall during the GFC, however, so we need to take this significant rise in investor market share lightly when we’re using it as evidence of a housing bubble.

Poor Underwriting

Other than tight supply, the main pushback on the argument for a housing bubble is the fact that the underwriting appears to be much better than it was leading up to the GFC.

For the most part this is true but there are a couple of data points that are interesting so let’s take a look.

There are 5 main metrics to track the quality of underwriting:

- % Adjustable Rate Mortgage loans

Adjustable-rate mortgages (ARMs) allow a borrower to pay a much lower interest rate in the first several years of the loan. It resets to a higher rate later on. As prices or interest rates increase, it’s common for ARM originations to increase as well. Particularly in the higher price ranges.

In fact, this is exactly what we’re starting to see now that prices are sky high & interest rates have started to climb.

While the current % of ARMs (10% of recent applications) is the highest we’ve seen in 14 years, it’s nowhere near what it was leading up to the GFC (35%).

In fact, ARMs still only comprise 4.7% of total outstanding loans as of March 2022[7].Compare that to the 35% leading up to the GFC & it’s apparent that ARMs should not be a problem. It’s very unlikely we’ll get forced selling because their interest rate resets to a level that they can’t afford.

2. LTV/CLTV

LTV & CLTV stand for loan-to-value & combined loan-to-value, respectively.

The interesting thing here is that the avg CLTV of conforming loans was actually higher over the 2017-2019 period than it was leading up to the GFC. [8]Conforming loans make up the overwhelming majority of originations.

Because of the run up in prices over the past few years, these loans should have plenty of equity to absorb a moderate fall in real estate prices provided we don’t get a surge in layoffs.

In my opinion, That’s the x-factor which will determine if we get a crash in housing prices or not. If people keep their incomes flowing at pretty much the same level, they will be able to absorb some sizeable price drops without having to go into foreclosure like they did in the GFC. However, if layoffs surge, all bets are off.

Homeowners will choose to sell their property while they still have some equity in it, further increasing the inventory we’re already starting to see, & driving prices down.

3. Avg FICO

There’s no doubt that FICO’s have improved significantly.

Keep in mind however, that there have been moratoriums on late charges & fees, evictions, student loan payments etc. Therefore, this may not show the true story. Had the moratoriums not been in place in 2020 when millions of people we’re laid off, late payments & evictions would have skyrocketed which would absolutely have reduced credit scores.

4. Avg Debt to Income Ratio (DTI)

Debt to income ratios are just about the same as leading up to the GFC. Problem is that this also has been affected by the moratoriums & stimulus payments.

Notice the large spike in the jumbo loan DTI’s. That’s interesting

5. Cashout Refi’s

Cashout refi’s aren’t nearly as large a portion of total originations as leading up to the GFC, but we have seen a fairly significant increase over the past year or so. We’ll have to keep our eye on that.

According to Blacknight, a mortgage data tracking firm, homeowner equity is at an all-time high & about double what it was leading up to the GFC.

Additionally, homeowners have been extracting only about 6% of their equity over the past several years. This is much lower than the 16% leading up to the GFC.

Because of this, most analysts conclude that the increase in cashout refi’s should not be a problem.