Originally, banks were not allowed to expand across state lines. Starting around 1980, states began to loosen these restrictions. This set off a 20+ year trend of larger banks buying up their smaller competitors for their deposit base, technology, brand, location and to squash competition.

Starting with the Citicorp and Travelers merger in 1998, and the eventual repealing of the Glass-Steagall Act in 1999, banks began acquiring and merging with investment/brokerage firms. They could now profit off the origination of loans and then profit off the securitization and sale of the same loans, wiping their grubby hands clean of any direct risk from a default.

Banks had been lobbying for a loosening of Glass-Steagall restrictions since the 1960’s!2

With their massive size, such behemoths became “too big to fail”. As of 2014, the 5 largest banks (the top 0.1% out of 6,509 total institutions) controlled 45% of total assets.4

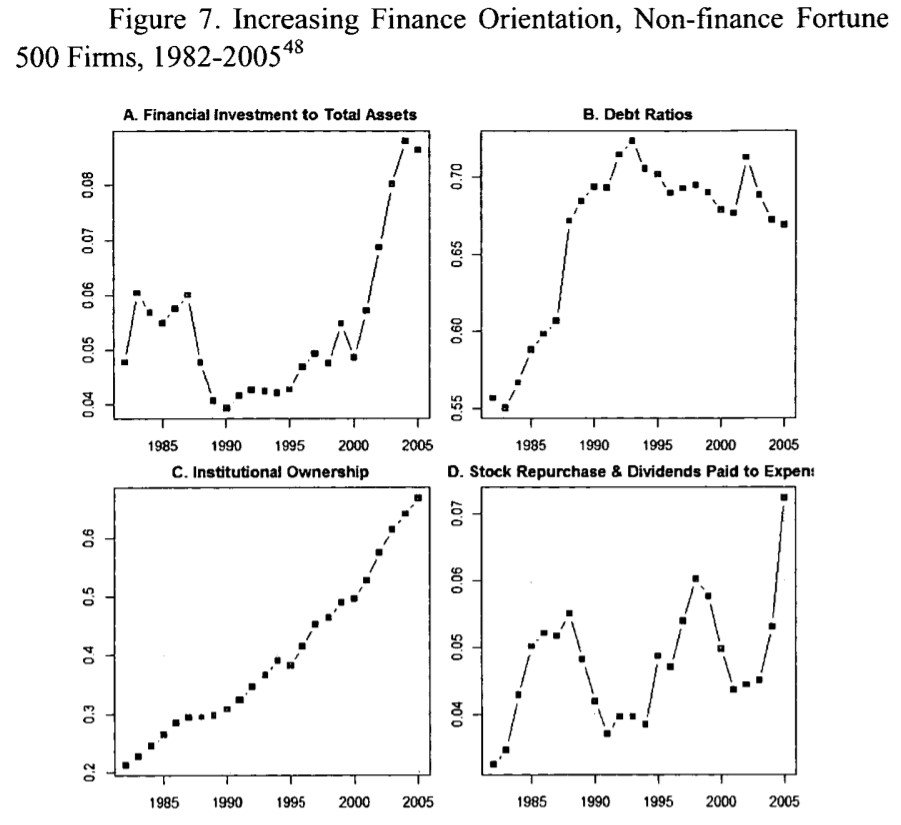

As the culture of financialization gained steam, the focus became short term profits and the maximization of shareholder returns. Investment in long-term productivity and output took a back seat to moving money through the financial system.

“Established [non-financial] firms [became] less and less treated as production units, but as bundles of tradable assets. Profits flow increasingly from financial investments, rather than trade in goods and services.”3

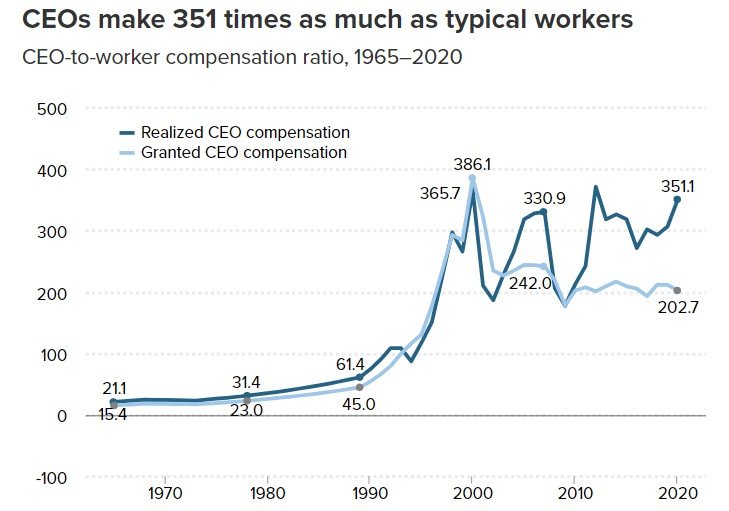

This short-term focus on shareholder returns also led to the explosion of stock options and other awards added to already lavish executive pay.

Stock options incentivize a focus on increasing the stock price as much as possible and as quickly as possible. Once the share price is above the strike price, executives can sell and pad their pockets with additional income.

Even worse, if you hold the stock for at least one year, you only have to pay 20% in federal capital gains taxes. Compare that to the 37% you’d have to pay if it were treated as ordinary income. This is a lower rate than someone making $80k per year pays on their income. In other words, you could be making $10 million per year, be given $1 million in stock options for free, recognize a $1 million profit by selling the shares, and pay as much tax as someone making $80k per year!

Needless to say, such schemes worsen the inequality between executive pay and that of the typical worker.

Debt is the hook of financialization. Like a drug, a little bit can be healthy and keep you balanced (think alcohol and weed). With 9:1 leverage, which isn’t hard to get using options or other derivatives, a 10% return on that investment doubles the amount you put in.

When times are good, scoring these types of returns leads to the desire for more. Greed drives you to repeat the process if it worked the first time. As long as the market is going up, everything is good. However, just as a 10% return can double your money, a 10% loss can wipe you out.

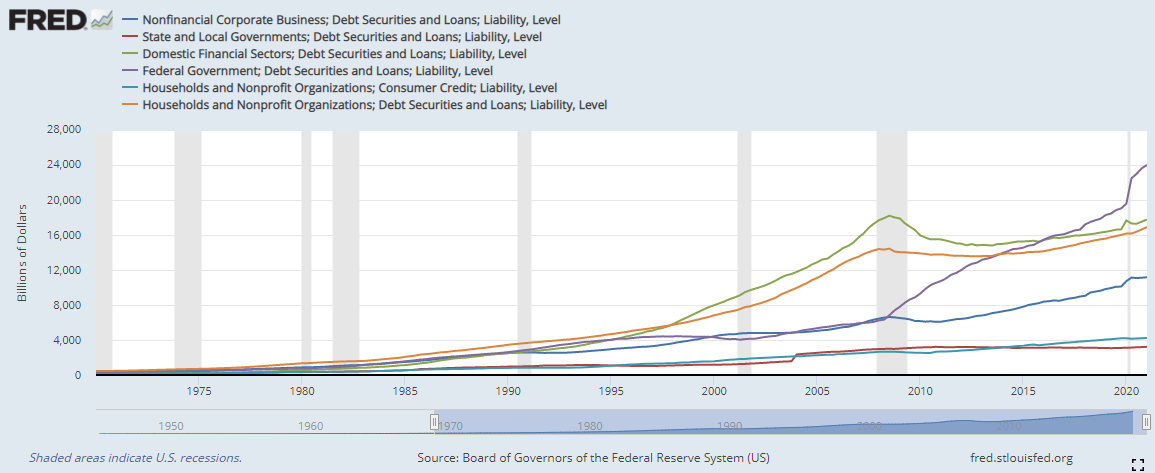

This is the power of debt. It can make you rich quickly, but it can also wipe you out just as quickly. The primary users of these types of strategies are the financial corporations but households and non-financial firms have also caught the leverage bug.

Can you guess the primary source of leverage for households? It’s by far the biggest source.

Mortgages!

The government-backed reduction in down payment requirements has resulted in the ability to put 3% down. That’s a 33:1 leverage on something that costs around $300k. A mere 3% return doubles your investment (the $9k down payment). It becomes obvious why house prices have shot up and the orange line in the chart below is one of the highest.

It sure looks like we’re all hooked!