those yourself by:

- Knowing the purpose of the investment in your portfolio

- Discerning what the investment does and does not do well.

- Understanding the micro economic picture such as the financial position of the company, company and industry trends, default risk, valuation risk etc.

- Understanding the macro economic picture such as inflation expectations, interest rates, currency risk etc and how those will affect the value of your investment.

- Read, read and read some more about the prospective investment.

I will expand on this as we go but first, let’s review the investment industry’s risk assessment methodologies. The next time you get an investment proposal covered with these volatility metrics, you’ll know what you’re looking at, how to interpret them and what they’re good for.

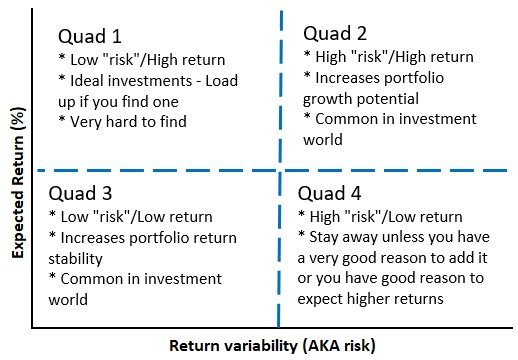

Ideally, you want to be on or above the line In the chart above. If you’re below the line, the variability of your returns is higher than your expected return.

Oddly enough, a majority of investments fall in sections 4 and 5 (below the line). Even stocks, the best performing asset over the past 100 years, fall in section 4.

As I mentioned before, we want to find investments that generate as high a return as possible for a certain level of “risk” (variability of returns and loss potential). In order to find such investments, we need to look at risk adjusted returns.

A risk adjusted return is simply the historical return divided by a risk measurement over the same time frame. this fraction is interpreted as an estimated return per unit of risk. These metrics can be used to make high-level comparisons between different types of investments.

Absolute Return

Absolute Return is simply the % change between your initial investment and the ending value of your investment over a specified period of time.

This is the basis for all other return calculations.

The main drawback of the absolute return is that it doesn’t take return variability, compounding or sequence of returns into account.

Average Return

Average Return is exactly what it says it is. Instead of taking the change in value over a long period of time, you take return measurements over a shorter period of time (daily, monthly or annually), and then you average them.

Let’s say you want to look at 3 year returns. You could calculate the return (using the absolute return formula) on a daily basis (756 measurements), monthly basis (36 measurements) or an annual basis (3 measurements). Then you take the simple average of your measurements.

The main drawback of average return is that it ignores the effects of compounding.

Trailing Return

Trailing Return is an average return calculation but instead of taking the average of smaller intervals, you calculate the absolute return over the longer time period and then divide by the number of periods.

The most important difference between trailing and average returns is that trailing returns do not take variability of returns into account.

The main drawback of trailing returns is that it does not take compounding or sequence of returns into account.

Annualized Return

To annualize something is to multiply the number by a factor that converts it to a 12 month basis.

For example, if you took a measurement over a 3 month period, you would multiply that result by 4 (there are 4 groups of 3 to get to 12) and the result would be the annualized rate. So a 3% return over 2 months equals an 18% annualized rate (3% * 6 = 18%).

This method ignores compounding but does account for the variability of returns.

Compound Annual Growth Rate (CAGR)

This is the rate of constant compounded growth required to get you from your initial investment to your current value.

It is derived from the Future value formula FV = Current Value * (1+ r)^n. All you do is algebraically manipulate the equation to solve for r.

In my opinion, this is the best return measure to use for investment performance purposes because It directly accounts for the benefits of compounding.

The main drawback of CAGR is that it does not account for variability or sequence of returns.

You can pair CAGR with a variability measure such as standard deviation, just make sure that both calculations use the same time frame.

Standard Deviation

Standard deviation measures the variability of returns around the average over whatever period your return data covers. You should always know the average return and standard deviation of an investment.

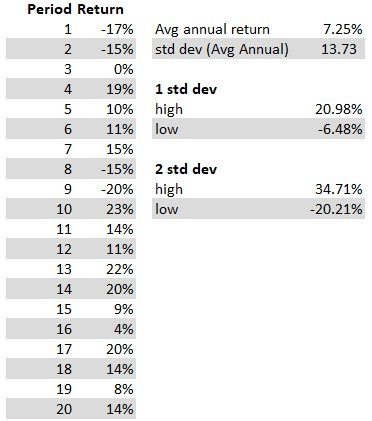

Let’s say you are looking at an investment with the following 20 years of returns:

Over this 20 year period the investment has averaged a 7.25% return per year with a standard deviation of 13.73.

There is a basic statistical fact that states:

- 66% of the time, future expected returns will fall with in 1 standard deviation from the average

Take the average return and add (1 * std dev) to get a high threshold and subtract (1*std dev) to get the low threshold.

- 95% of the time, future expected returns will fall with in 2 standard deviations from the average

Take the average return and add (2 * std dev) to get a high threshold and subtract (2*std dev) to get the low threshold.

Applied to the data above, we can expect our return to be anywhere from -6.48% to 20.98%, 66% of the time. Likewise, we can expect our return to be anywhere from -20.21% to 34.71%, 95% of the time.

Besides the backwards looking nature of the standard deviation, another draw back is that it estimates the variability to the upside as well as the downside of the average return.

But as investors, we don’t consider a higher return than expected to be a risk. That’s what we want! That brings us to 3 other measures of return variability (“risk”).

Beta

Beta is a measurement of the change in your target investment relative to the change in some benchmark/Index. For stocks, that benchmark is something like the S&P500, the Nasdaq 100 or the Russell 2000. The benchmark for bonds can be treasuries or other bonds similar to your investment.

If your investment has a beta of .80 that means for each 1% change in the benchmark, your investment is expected to change by 0.8%. It works on the upside as well as the down side.

Beta < 1: Your investment will gain less and loose less than the benchmark most of the time.

Beta = 1: Your investment usually moves in lock step with the benchmark.

Beta > 1: Your investment will gain more and loose more than the benchmark most of the time.

Beta is primarily used as a gauge of market risk. But you must understand what benchmark you are comparing it to for it to be a valid piece of information.

I prefer to look at the return variability of the actual investment I’m interested in, but Beta can be useful when you don’t have access the actual returns of your investment. The logic is that if you are familiar and comfortable with the variability of the benchmark, and if the Beta of your target investment is close to 1, you can be pretty sure you’ll be comfortable with the variability of the investment; Depending on your objective of course.

To find something that is less variable, you’d look for an investment with a lower Beta.

Upside/Downside Capture

Like Beta, it is also a comparison of your investment to a benchmark.

The capture ratios show you historical performance of your investment on up days (upside capture) and down days (downside capture) with the benchmark being a value of 100.

Upside capture of 110 means that, on average, your investment will go up 110% of the change in the benchmark (benchmark + 10%) on up days.

Downside capture of 90 means that, on average, your investment will go down 90% of the benchmark (benchmark – 10%) on down days.

You want to minimize the downside capture and maximize the upside capture.

% of down periods or periods not beating inflation

This is one that I like to look at but it’s not found in any metrics commonly reported that I’ve found. You will have to calculate it your self.

It’s simply the % of time over a certain period that your investment has had a negative return or failed to return more than inflation.

Using the data in the standard deviation section above, you can see that out of the 20 years data we have, the investment has had 4 years with negative returns (20% of the time). About 1 in every 5 years, the investment loses money.

Extend this to look at the # of years that the investment didn’t beat inflation and you see that this has been 5 years out of 20 (25%).

You need to then determine if you are comfortable with those chances. You can also calculate the avg. return in those down years to get an extremely rough estimate of what type of loss you could expect should your investment not beat inflation.

For better estimates as to how big of a loss is possible at any given moment, check out Value-at-risk (Var) and Conditional Value-at-risk (CVar).

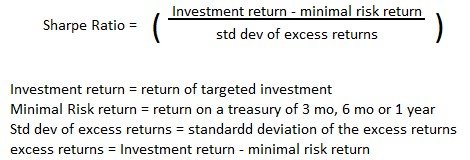

This metric measures the excess return per unit of “risk”.

The excess return is the return received above the least risky alternative (usually short term treasuries), while the “risk” is simply the variability of the excess returns.

In general, you want a Sharpe Ratio >= 1. A Sharpe < 1 means that an investment’s excess return is lower than the variability of those excess returns. In other words, the investment was not able to generate enough excess return to compensate for the “risk” you took.

The use of the standard deviation as the denominator treats all excess return variability the same. In other words, returns higher than the low risk rate are just as unwanted as returns lower than the low risk rate.

Anyone with a brain understands that returns above the low risk rate are desirable while returns below the low risk rate are not. This is one of the drawbacks of the Sharpe Ratio.

Alpha

Alpha is similar to the Sharpe ratio in that it looks at excess returns. But instead of comparing an investment’s return to that of a low risk investment, it compares it to both a benchmark/index and the low risk investment.

Unlike the Sharpe Ratio, this metric only measures the variability due to the market.

As discussed earlier, Beta is the return variability of an investment relative to that of a benchmark/index.

Alpha is most commonly used in conjunction with Beta and is applied to a portfolio (your portfolio, mutual fund, ETF etc) rather than a single investment.

In general, you want an Alpha >= 0. This means that the investment’s return was high enough to compensate for the risk associated with market conditions.

An Alpha < 0, means that it did not achieve a high enough return to compensate for the market/benchmark “risk”.

A low risk investment is a 3 month, 6 month or 1 year treasury.

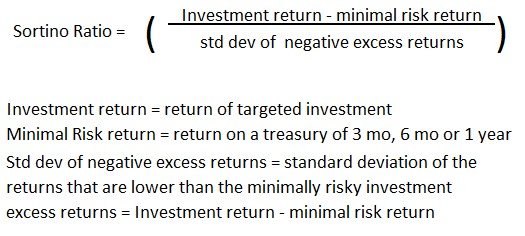

Sortino Ratio

The Sortino Ratio is also similar to the Sharpe Ratio in that it looks at the excess returns vs a low risk investment and is interpreted as a return per unit of “risk”.

Like the Sharpe Ratio, this metric considers risk from all sources not just the market.

But, unlike the Sharpe Ratio, which treats both positive and negative excess returns as equally undesirable, the Sortino Ratio focuses only on the negative excess returns; More in line with the true goals of investing.

Just like the Sharpe ratio, you want a Sortino Ratio >= 1.

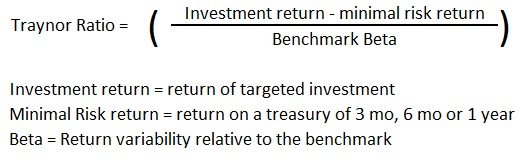

Treynor Ratio

Yet another variation on the Sharpe ratio, this one combines the ideas of the Sharpe ratio and Alpha. It takes the excess return and adjusts it per unit of market “risk” as measured by Beta.

As discussed before, Beta is a measure of variability relative to a benchmark/index and therefore only captures risks related to the market.

In general, you want a Treynor Ratio >= 1.

A Treynor Ratio < 1 means that the excess return is not enough to compensate you for the market “risk” as measured by Beta.

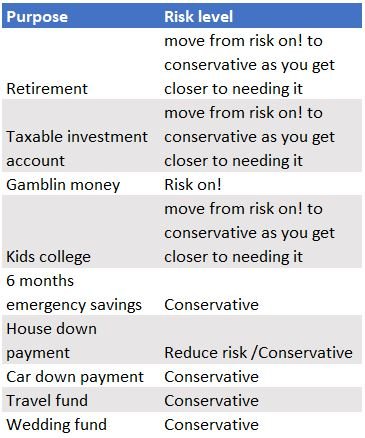

What is the $ for?

Money that is needed in the next 2-3 years should probably be held in more conservative investments such as high yield savings accounts or money market mutual funds/ETF’s.

Down payments on a car or house, savings for children’s college that will be used in the next year or two, savings for your upcoming wedding, a travel fund etc., are all instances where you’d want to be more conservative with that money.

Your ability to be conservative with the money is highly dependent on the inflation rate.

If inflation is not a problem and you can maintain your purchasing power by keeping the money in ultra-safe investments, then it’s usually the best to do so.

On the other hand, if the prices of the items that you intend to spend the money on are increasing faster than the interest rate you’re receiving in conservative investments, then you almost have to consider keeping at least a portion invested to try to maintain your purchasing power.

The percentage is up to you but in most circumstances it’s probably smartest to keep at least 40-50% in safe investments unless inflation is super high, like 10% or more.

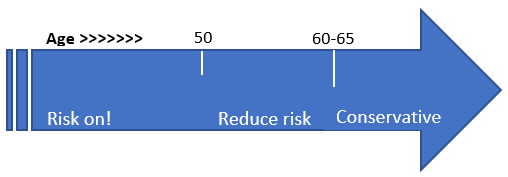

How long until you need the money?

If you are young and don’t need the money for a long time (retirement money), then mathematically speaking, you can afford to have a fairly large portion of your portfolio allocated to riskier investments offering higher returns.

If you receive poor returns for a few years (even 5 years), you’ll have plenty of time to recover.

The older you are, or the closer you get to needing the money, the generally accepted wisdom is to reduce risk. It’s wise to allocate a smaller portion to riskier assets and to increase your allocation to safer assets like cash, money market funds and/or bonds.

Can you stomach the risk?

Are you a person who can ignore market fluctuations and hold on for the long term?

If so, there is nothing wrong with taking on risk in pursuit of higher returns. As always, make sure you understand the risks and have a backup plan incase it backfires and ends up costing you money that you should have been protecting.

A useful exercise is to ask yourself, If I lost 40% of this money:

- Would it severely affect my daily financial situation?

- Would it cause undue stress and negatively affect my health or happiness?

- Would it jeopardize the goal for which I’m investing?

If you answer yes, to any of these questions it’s probably too much risk for you.

Ask yourself the same questions if you lost 25% of the money, and again if you lost 15% of the money and so on.

Generally, you have to be willing to take a 30% loss to invest in the stock market. Most of the time you will make money, especially over long periods of 10 years or more, but big losses do come around once every 10-15 years.