Bad Assumptions Lead to Bad Conclusions

The right side (M*V) is where the Equation of Exchange breaks down. It makes two assumptions that have little evidence to support them.

We can accurately measure the money supply

The fact we’ve changed money supply measurements (M1, M2, M3 etc.) should be a clue that we aren’t entirely sure how to define money as it pertains to output.

Originally, we relied on M1 as the official measure of the money supply. However, “financial innovation posed problems for monetary measurement, as banks introduced new types of accounts that blurred the distinction between transaction deposits and other types of deposits. To accommodate these innovations, alternative definitions of money were created; By 1971, the Federal Reserve published data for five definitions of money.” 1

M1 was eventually ditched for a wider measure called M2 because the relationship between M1 and output broke down. The relationship between M2 and output has also broken down over the past 30 years leaving us in a similar situation.

One thing has become clear. Behavioral dynamics, financial innovation, and changing incentives imposed by regulations, often leads to changing forms of money. Since we haven’t been able to develop a measurement that dynamically adjusts to these changes, we haven’t been able to find a reliable relationship between our money supply measurements and output. As a result, we’ve relied on a calculation referred to as the velocity of money to capture this relationship.

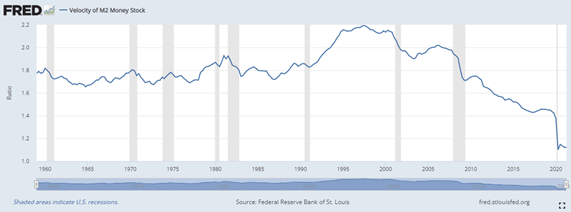

The velocity of money is measurable

The most common mistake while using the Equation of Exchange is to treat the velocity of money (V) as an independent variable that we can measure. In reality, nobody has come up with a way to actually measure the velocity of money. Instead, we algebraically derive it as V = (P*Q) / M.

In other words, the velocity is nothing more than a calculation. Once you understand this, it is no wonder that a spike in the money supply, without a corresponding spike in output, leads to a drop in the velocity of money.

Instead, velocity should be viewed as a black box that captures all the things that can affect the relationship between the money supply and output. It’s kind of like Total Factor Productivity that relates output to labor and capital in the production function.

Velocity is a catch all that includes things such as:

- Errors in our measurement of the money supply or output

- Financial innovations that change the forms of money

- Regulations that change consumer and business behavior

- Social changes that affect where and how wealth is stored or drawn upon

- True changes in the velocity of money

- Debt levels and it’s impact on consumer and business behavior

- The demand for money relative to the supply

- The wealth effect

These two assumptions lead to two conclusions which have been falsified over the past 20 years. First, an increase in the money supply without a corresponding increase in output will necessarily lead to an increase in inflation. It definitely can, but quantitative easing has proven that this is not always the case. Second, the unwillingness of consumers and business to spend is the reason that increases in money supply has not led to runaway inflation.

Even though the Equation of Exchange has it’s shortcomings, it’s still a valuable theory to grasp the high-level relationships between money and output.